Young Adults Are on an Uncertain Road to Retirement

LOS ANGELES – Jan. 28, 2021 – With increasing strain on social security systems globally and the economic effects of the pandemic intensifying, young adults are setting out on an uncertain journey of work and money. They are expecting to self-fund an even greater proportion of their retirement income than previous generations. However, few young adult workers (age 20 to 29) think they are on course to achieve their retirement income needs (20 percent global, 26 percent U.S.), according to a report released today, The New Social Contract: Young adults reinventing life, work, and retirement.

“Navigating our 20s was a struggle before the pandemic. Now, many of us are in a more precarious financial situation. From high rates of student debt and unemployment to unaffordable housing, a variety of factors are stacking against young Americans’ ability to achieve long-term financial security,” said Heidi Cho, a millennial retirement expert for nonprofit Transamerica Center for Retirement Studies®.

The new report explores retirement related attitudes and behaviors of workers in their 20s, a cohort straddling Millennials and Generation Z. The survey spans 15 countries in the Americas, Europe, Asia, and Australia. It was conducted during January and February 2020 at the onset of the pandemic and is a collaboration among nonprofit Transamerica Center for Retirement Studies® (TCRS), Aegon Center for Longevity and Retirement (ACLR), and Instituto de Longevidade Mongeral Aegon.

Life Priorities, Financial Priorities, and Retirement Preparations

“Young adults are reinventing life, work, and retirement to infuse flexibility. With the potential to live longer, we have more time to pursue our passions, embark on different careers, and possibly take gap years,” said Cho.

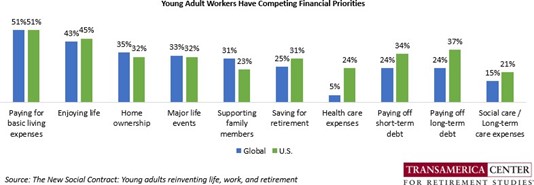

Young adult workers are juggling a variety of life priorities including their careers (53 percent global, 56 percent U.S.), enjoying life (53 percent global, 59 percent U.S.), and planning for their financial future (53 percent global, 62 percent U.S.). At the same time, they face competing financial priorities including paying for basic living expenses, enjoying life, home ownership, major life events, supporting family, and paying off debt.

While relatively few young adult workers cite saving for retirement as a financial priority, many have already begun thinking about retirement. The survey finds encouraging news that 32 percent of young adult workers globally are “habitual savers” who make sure they are always saving for retirement (40 percent U.S.). Globally, 17 percent of young adult workers have a written retirement strategy and 42 percent have an unwritten strategy (25 percent, 31 percent respectively U.S.). They estimate that more of their retirement income is likely to come from their own savings and investments (36 percent global, 35 percent U.S.) and the government (36 percent global, 34 percent U.S.), than from employers (28 percent global, 32 percent U.S.).

The life journeys of young adults require an increasing do-it-yourself approach to retirement preparations, especially given their job-hopping tendencies and expectations. More than half of young adult workers say the longest period of time they have worked for, or expect to work for, any single employer is one to five years (52 percent global, 59 percent U.S.).

“Saving for retirement may be the last thing that comes to mind for young Americans, especially amid the pandemic. However, it is important that everyone begins saving and planning as early as possible to benefit from the long-term compounding of investments over the course of our lives,” said Catherine Collinson, CEO and president of nonprofit Transamerica Institute® and TCRS, and executive director of ACLR.

How Employers Can Support Young Adult Workers

Employers play a highly influential role in facilitating retirement preparations for workers. When asked what prompted them to start saving for retirement, young adult workers more often cite employer-related reasons (49 percent global, 52 percent U.S.), such as starting a job, the offering of retirement benefits, automatic enrollment, and/or receiving a raise or promotion, than life-stage related reasons (44 percent global and U.S.).

Employers can help their young adult employees by offering meaningful work experience, competitive compensation and benefits packages, flexible work arrangements that support work-life balance, and training and development programs. Because young adults are more likely than preceding generations to switch careers, change employers, and possibly spend time in self-employment, they need portable health, welfare, and retirement benefits that they can maintain on their own after they separate from an employer.

“Young Americans should join together and make retirement savings a priority, raising our voices and demanding a concerted effort among policymakers, industry, and employers to ensure generational equity in Social Security and a modernized retirement system that will serve us and future generations of retirees,” said Cho.

The New Social Contract: Young adults reinventing life, work, and retirement contains in-depth analysis, country- specific comparisons, and detailed recommendations for young adults, employers, and governments. It is based on findings from the 9th Annual Aegon Retirement Readiness survey. Please visit www.transamericainstitute.org to download the report and other global retirement research in The New Social Contract series. Follow TCRS on Twitter @TCRStudies.

Transamerica Center for Retirement Studies

Transamerica Center for Retirement Studies® (TCRS) is a division of Transamerica Institute®, a nonprofit, private foundation. TCRS is dedicated to conducting research and educating the American public on trends, issues, and opportunities related to saving, planning for, and achieving financial security in retirement. Transamerica Institute is funded by contributions from Transamerica Life Insurance Company and its affiliates and may receive funds from unaffiliated third parties. TCRS and its representatives cannot give ERISA, tax, investment or legal advice. www.transamericainstitute.org

274623 01/21